Benchmarking the Status of Buy Indian Act Implementation

The Buy Indian Act (25 U.S.C. § 47) is important for advancing economic development and self-determination in Indian Country. There was a considerable amount of change over the last year, which can have an impact on actual acquisition obligations, including those related to the Buy Indian Act. This post will look at Buy Indian Act award trends within Indian Affairs (Bureau of Indian Affairs, Bureau of Indian Education, and Bureau of Trust Funds Administration) and the rest of the Department of the Interior. It’s a good time to lay down some benchmark data we can return to in the future to review performance and policy changes. Amidst a lot of change, one possible lesson is strong underlying business practices and use of smart procurement vehicles can make a difference even within the swirl of change.

Background

The Buy Indian Act (25 U.S.C. § 47) statutory requirements and supporting regulations authorize Indian Affairs and the Indian Health Service to give preference to qualified Indian Economic Enterprises when purchasing supplies, services, and construction activities.

Indian Affairs and IHS have taken steps to broaden the authority's impact through regulatory improvements. Additionally, over several years, Indian Affairs implemented proactive education and development of smart acquisition tools to make choosing a vehicle that supports the Buy Indian Act a good decision to meet procurement goals and be operationally effective.

So, what changed in FY 2025?

We’ll look at a couple of layers of data to see what kind of story we can tell. First, we’ll look at acquisition obligations across Interior.

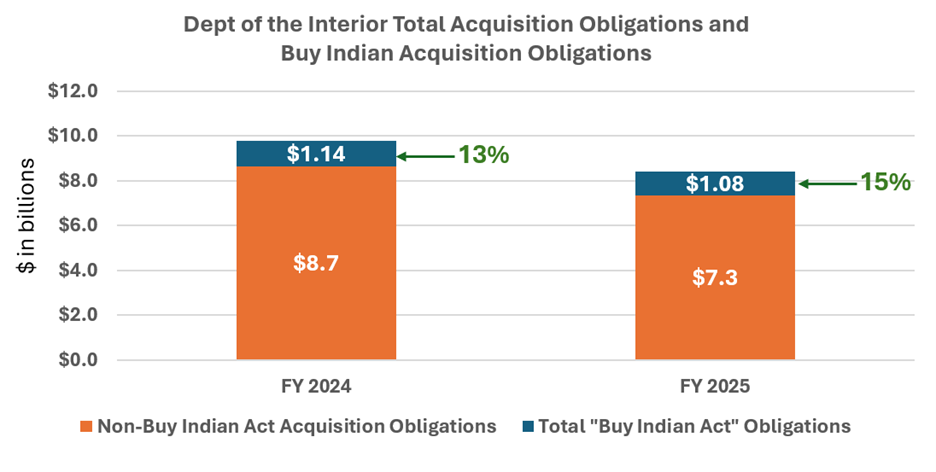

Interior acquisition obligations as a whole dropped by $1.4 billion, while Buy Indian Act obligations declined by $60 million. As stated above, there are many reasons for acquisitions to drop, including new approval review processes, a very late appropriation, and staffing reductions.

While overall obligations decreased, the percentage of total Buy Indian Act obligations compared to total obligations increased in FY 2025. This may be a good sign that the smart acquisition vehicles created by Indian Affairs remain a strong option for managers across the Interior to support effective operations. Additionally, the tools and education provided by Indian Affairs to vendors such as the Buy Indian System for Award Management continue to help Indian Economic Enterprises identify procurement opportunities.

Graph based on Indian Affairs data from the Buy Indian Act Information and Tools webpage.

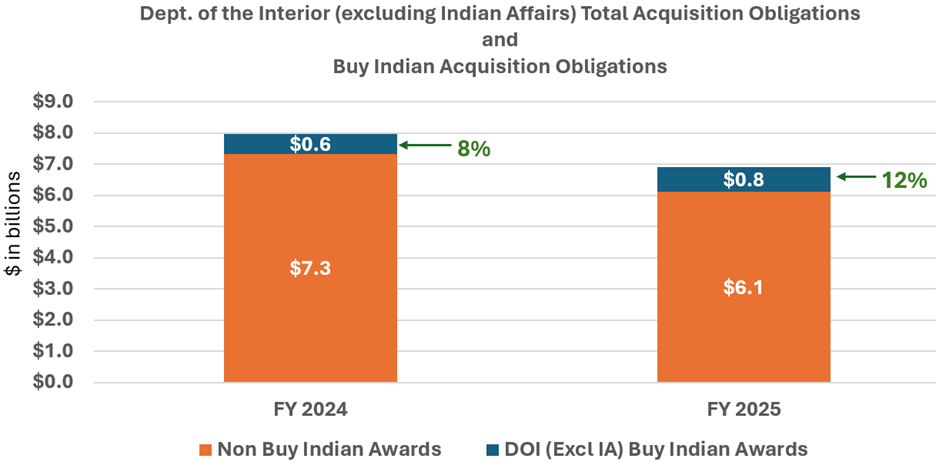

It helps if we dive a bit deeper into the data and focus on acquisition obligations for Interior bureaus outside of Indian Affairs. Interestingly, other Interior bureaus actually increased their Buy Indian Act obligations in FY 2025 by over $170 million, despite an overall reduction in total obligations. Difficult to pinpoint why, if I had to guess, it's likely some bureaus used Indian Affairs smart acquisition vehicles for construction purposes – one or two projects in this area can result in a big change in obligations. But it could be due to other factors. These acquisition vehicles have been well received by other Interior organizations and can also be used by the Indian Health Service.

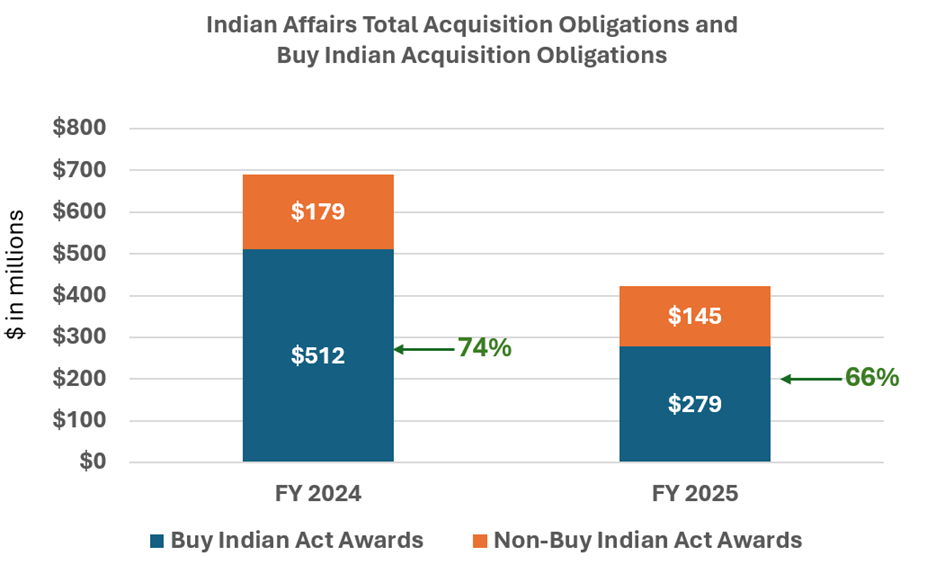

Last, we take a look at acquisition obligations within Indian Affairs. Total acquisition obligations dropped in FY 2025 by $268 million, and Buy Indian Act obligations dropped by $233 million. The percent of total obligations supporting Buy Indian Act awards dropped from 74% in FY 2025 to 66% percent in FY 2025.

Why the change?

I’d turn to the usual suspects of additional approval processes, fewer staff, and late appropriations as major factors. Like other parts of DOI, construction is often a big swing factor in Indian Affairs acquisition obligations. One construction project not making it through the acquisition process before year's end can easily result in a $100 million or more swing in total obligations.

The expiration of the Great American Outdoors Act Legacy Restoration Fund, which provides $95 million a year for BIE School Construction, could also contribute to the lower levels. The LRF expired at the end of FY 2025, so no additional funds would have been available in FY 2026. LRF funds are often critical to ensuring sufficient resources on hand to advertise a procurement opportunity for BIE construction projects. Fingers crossed, the LRF is reauthorized later this year to support the continued modernization of BIE schools and address the maintenance backlog.

Moving forward

It will be important to continue tracking trends in Buy Indian Act data, as well as any changes in policy. The regulations and policies in place, as well as the strong use of smart acquisition vehicles and educational outreach efforts, have enabled Indian Affairs to make the implementation of the Buy Indian Act an economic win for Indian Country and to help leaders at other Interior bureaus and the IHS advance more effective operations.

Increasing Transparency, Trust, and Relationships in the Budget Process

The FY 2026 budget justification documents for Indian Affairs, as well as other Interior agencies, did not include critical information typically available to support meaningful consultation with Tribes and engagement with Congress on appropriately and accurately funding bipartisan priorities, such as law enforcement. This lack of transparency was further complicated by the fact that the Indian Affairs FY 2025 Budget Operating Plans were not made available to Congressional staff or Tribes. The lack of detail doesn’t just impact budget decisions, it also complicates the ability of Tribes to deliver services on behalf of the Secretary of the Interior in support of Indian self-determination contracting and self-governance compacting.

OMB’s decision to strip budget detail is largely based on the goal to increase Executive Branch control over funding allocations. On its own, the separation of power regarding Congress’s authority to appropriate funds is a major issue that the Appropriators pushed back on in the FY 2026 conference bills. But OMB’s actions also circumvent the spirit of consultation and partnership with Tribes who perform critical services on behalf of the Secretary of the Interior. The data are in many ways an essential glue that trusted relationships and communications are built on during the appropriations process.

The information below describes what information is no longer available in budget justifications, why it matters, and what should be done next. It's clearly time for the Federal government to modernize how we communicate with Tribes and other citizens of our nation on the value of programs described in the budget, but this action to strip vital information is a step backward. There is time to take a step in the right direction with the FY 2027 budget, which should be released in the next two months.

What changed in budget justifications?

Change #1: Loss of program-level investment information

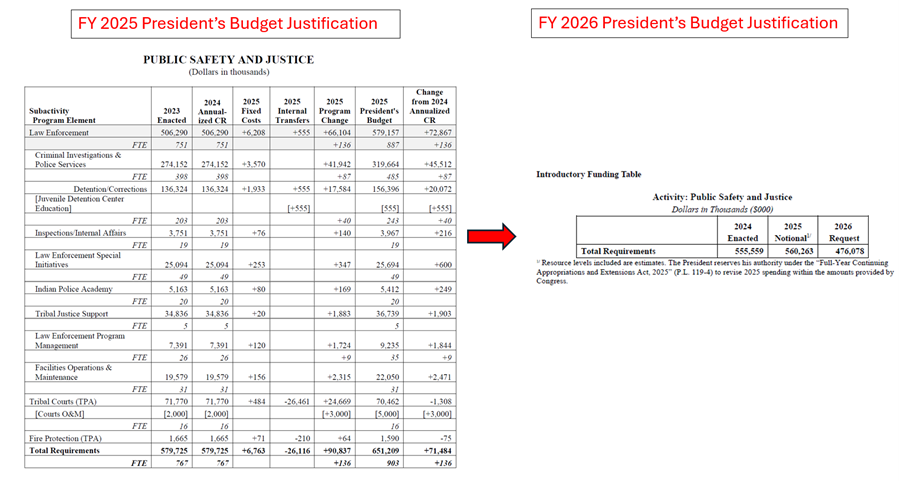

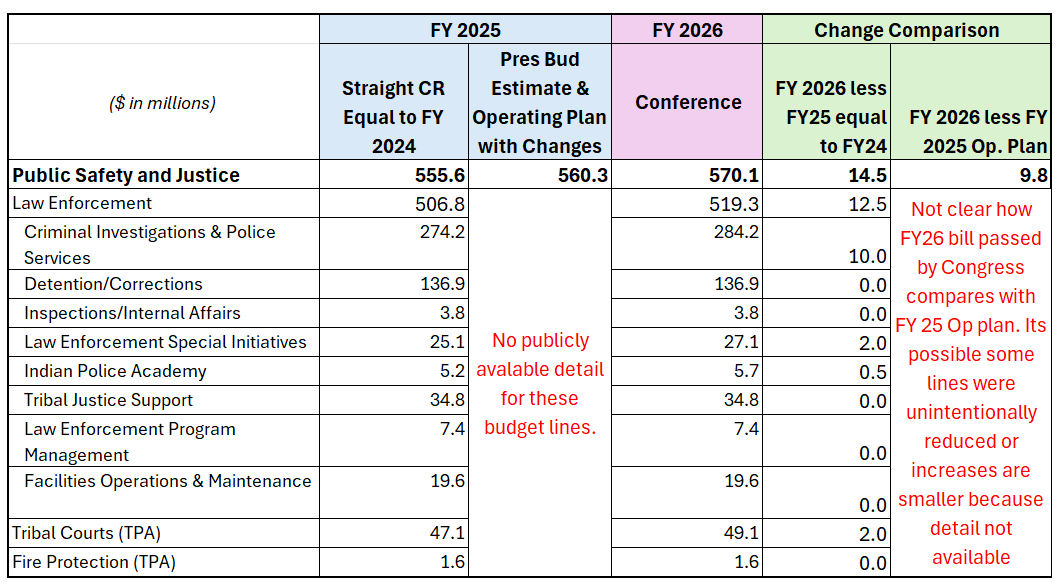

The FY 2025 Congressional Budget justification for Bureau of Indian Affairs and Bureau of Indian Education and the previous justifications for at least the last 3 decades included the budget Activity (Public Safety and Justice), the Subactivity (Law Enforcement) and Program Elements (Criminal Investigations and Police Services, Detentions and Corrections, Tribal Courts, etc). This information is necessary for Tribes and Congress to assess the Administration’s proposal and understand the level of funds they will receive to conduct contracted and compacted activities. The FY 2026 Budget Justification only provided a total amount of funding for all of Public Safety and Justice. The image below shows the change in level of detail.

Graphic compares level of level of budget detail provided in FY 2025 versus FY 2026.

Why does this lack of detail matter?

Undermines meaningful consultation with Tribes: Indian Affairs typically holds three consultations a year with Tribes on budget priorities, program implementation feedback, and technical questions. This interaction is critical for ensuring Tribal priorities are reflected in the President’s Budget request.

During meaningful consultation with Tribes on the Budget, it's often necessary to talk at the topline level and then dive into the particulars. If BIA can’t clearly answer questions about how much is assumed for criminal investigations versus detentions and corrections or Tribal courts and social services, the quality of discussion in consultation diminishes significantly.

Difficult for Congress to make informed decisions and have a shared understanding of support for priorities: The appropriators need detailed information to make decisions. For the FY 2026 appropriations bill, appropriators did not have a solid baseline to make decisions on, because the Administration did not provide a program-level detail on the budget for FY 2026, and did not share the FY 2025 Operating Plan, which agencies were directed to provide under the FY 2025 Continuing Resolution (PL 119-4).

As a result, appropriators made decisions about increases or decreases based on FY 2024 levels they had details on, or on the assumption that FY 2025 levels were equal to FY 2024. Especially given the high rates of turnover on the Hill, budget justifications have served as a form of historical memory. The loss of publicly available data and high turnover will put Congress at a significant disadvantage going forward. This situation could also lead to Appropriators and the Executive Branch, as well as the broader public, being ships passing in the night, talking past each other. Below is a table showing appropriators' intentions for law enforcement and possible disconnect that result from lack of data.

Topline confusion: Appropriators intended to provide an increase of $14.5 million in the FY 2026 bill, but when compared at the topline to the Administration’s movement of funds under an operating plan, it only results in a $9.8 million increase.

Program level allocation confusion: Because the appropriators did not have funding levels from the FY 2025 operating plan from the Administration, they do not know how their allocation compares to FY 2025. Indian Affairs clearly moved money from other parts of the budget to Public Safety and Justice in FY 2025, but it's not clear where they added it within Public Safety activities. For example, there are known needs in Tribal Justice Support and Detentions and Corrections (additional staff and contract beds). If Indian Affairs moved funding to these areas in FY 2025, the FY 2026 Conference decisions may have inadvertently cut funding in some lines. There are ways to fix this; if necessary, Indian Affairs can reprogram funding. But this can be time-consuming, and creates more uncertainty with Tribes who are contracting and compacting for these activities.

Increases uncertainty for Tribes who need to make decisions about hiring and other operational costs for their contracted and compacted programs. At the heart of effective self-determination contracting and self-governance compacting is the assumption that Tribes will conduct services BIA and BIE used to provide on behalf of the Secretary. Part of achieving an effective contracting relationship is ensuring Tribes have access to the same funding information that Indian Affairs bureaus have. Based on the significantly reduced level of detail available, this can make it harder for Tribes to manage programs and ensure they are receiving the correct amount of funding.

Major Change #2: Loss of historical information on Self Determination contract and Self Governance compact funding levels

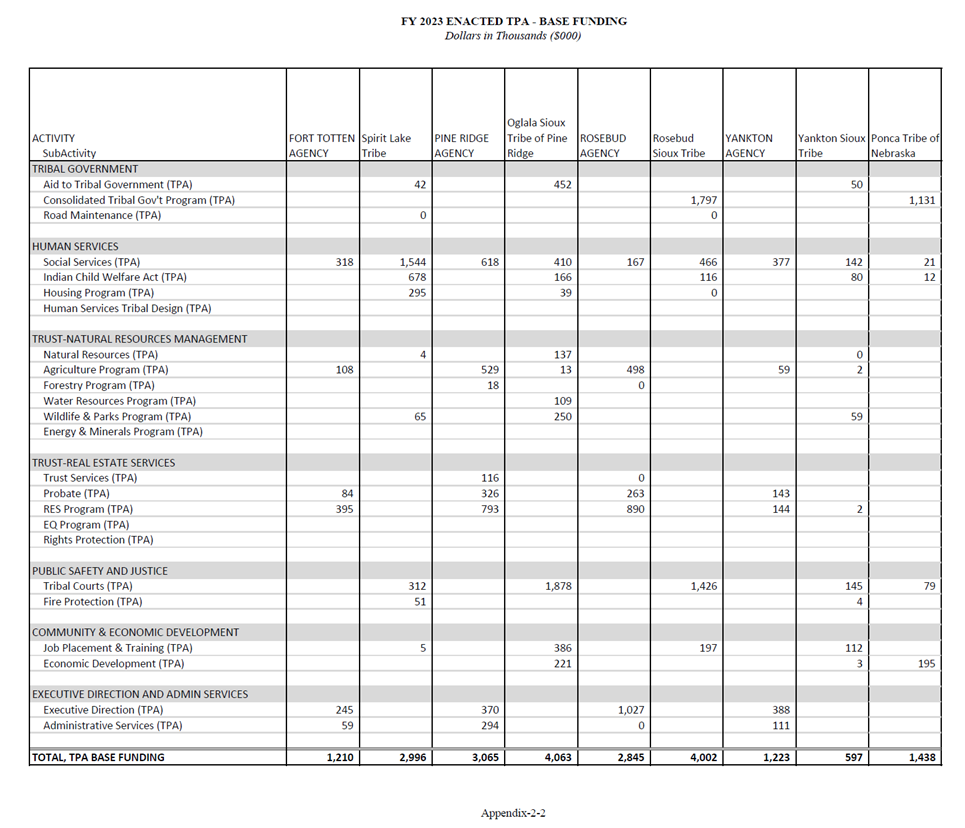

The BIA and BIE budget justification used to include tables in the Appendix for Tribal Priority Allocations by location. This table is critical for Tribes to confirm the TPA funding levels they are receiving and understand the direct services funding amounts by location in case they want to contract for more activities. The amounts in this table are considered annually recurring and don’t change unless Congress explicitly increases or decreases funding in an appropriations bill or Tribes move money across TPA lines. This information is even more important now as BIA has reduced its workforce. In FY 2027, funding from those employees who left Federal service should be considered as an option for more Tribal contracting. The administration has talked about expanding self-governance; making this information accessible would help that process.

Example from Appendix of FY 2025 President Budget Justification for BIA of a table that breaks out core Tribal government funding by Tribe and BIA agency. This data is critical for verifying funding levels for services. There is a similar Tribal Priority Allocation Table by Location in the Bureau of Indian Education for the two TPA programs they distribute, Scholarships and Adult Education and Johnson O’Malley.

Solutions for Moving Forward:

At a minimum, the detail that was stripped out (and additional examples provided as an addendum below) should be added back in the FY 2027 President’s Budget justification.

An actual step forward would be to shift these tables from their current static presentation in the budget justification into a searchable and sortable online product to facilitate review of funding levels by Tribes to improve implementation of contracted and compacted activities and advance self-governance more broadly.

ADDENDUM

Other examples of tables previously in the BIA and BIE budget justifications that facilitate Tribal contracting and compacting

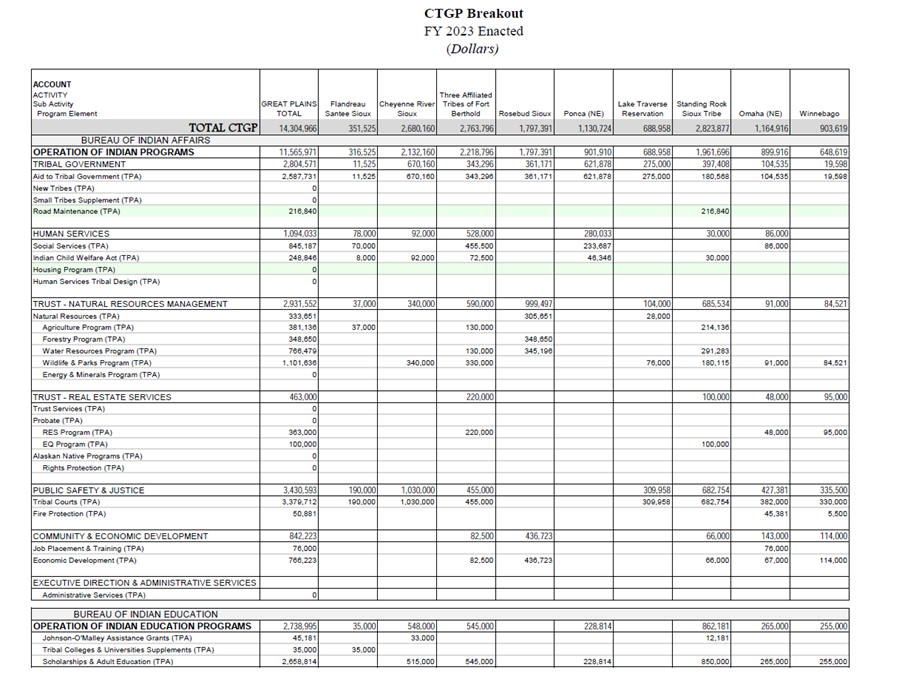

Consolidated Tribal Government Program (CTGP) Breakout. Under the CTGP line item, Tribes can merge and consolidate several programs into a single contract activity to engage in a simpler and more flexible method for setting priorities, goals, and objectives. The combination of activities of similar character gives Tribes the most effective means of setting priorities and operating programs consistent with Tribal goals and objectives, as well as with Federal laws and regulations. It is critical for Tribes to have access to this table to be on the same page with BIA regarding what program funding is merged into CTGP.

BIE Congressional Justification Budget Appendix Tribal Priority Allocation Table by Location. About 150 of the 183 BIE funded schools are Tribally operated. It is critical for Tribes to have access to formula distributions to ensure proper payments and understand BIE’s distribution methodology.

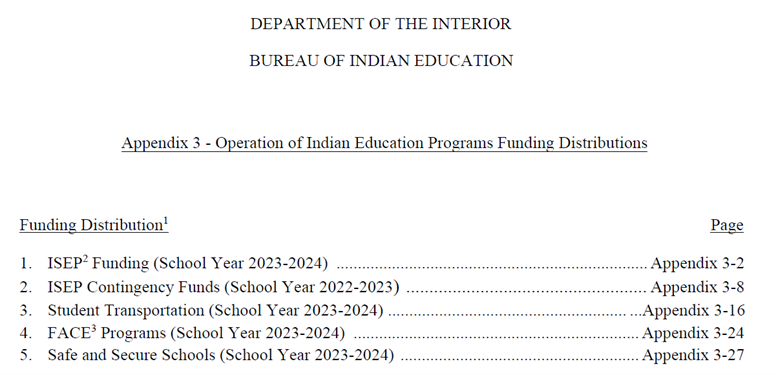

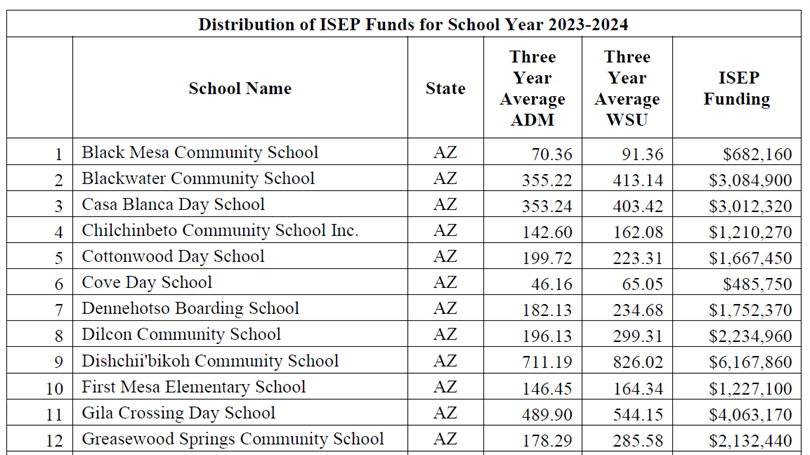

Indian School Equalization Program (ISEP) funding distribution. The Indian School Equalization Program (ISEP) funds most operating costs for BIE schools.

Distribution of SY 2023 -2024 Transportation Funds

This table provides the distribution of Student Transportation Funds to each school for the most recent school year.

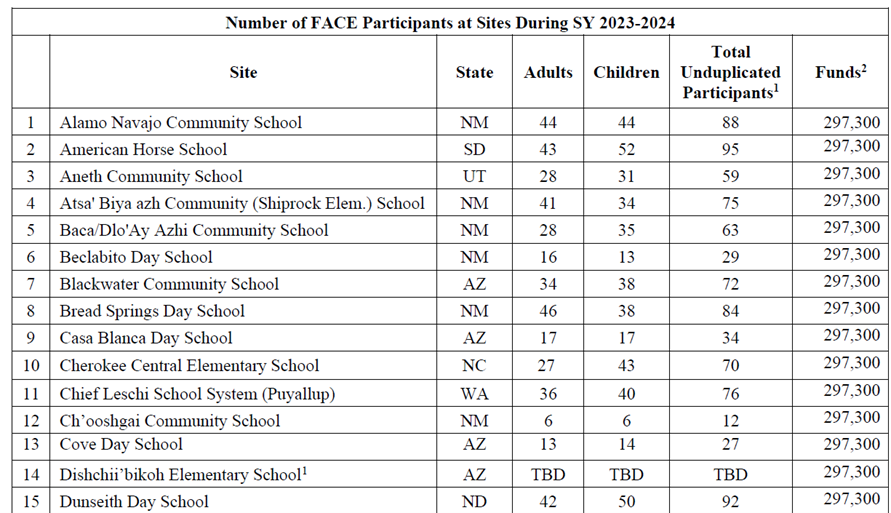

Distribution of FACE funds for School Year 2023-2024

This table provides school level funding allocations for the 54 schools that are part of the Family and Child Education (FACE) program. This program seeks to narrow the educational achievement gap for Indian children, particularly those in rural.

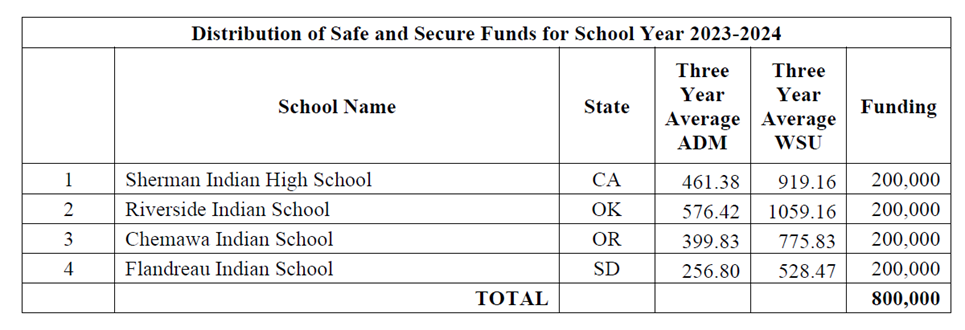

Distribution of Safe and Secure Funds for School Year 2023-2024

This table highlights funding provided to school programs identified as having high safety and security issues. These schools utilize the funds to support police and security services at off-reservation boarding schools with unique at-risk student populations and proximity to urban centers.

Budget Topline Issue #2, Urgent Displacing the Foundational - Indian Water Rights Settlements

For our next major budget topline issue, we’re focusing on Indian water rights settlements as an example of responding to the urgent resulting in displacement of foundational priorities. The Federal government is on the hook to provide more than $312 million by 2029 to meet the enforceability requirements of the Hualapai Tribe Water Rights Settlement Act (PL 117-349) and is increasingly facing a growing balloon payment. The Debt Ceiling deal with lower budget caps went into effect in FY 2024, constraining resources that could be available for the settlement. No significant funding has been appropriated since the settlement was enacted in 2023. As a result, there are now only three fiscal years (2027-2029) for the Federal government to cover the amount necessary to meet settlement enforceability requirements. The fiscal outlook does not look great in the future years, so this is not a challenge that will get easier with time.

Why is this such a challenge and what can be done?

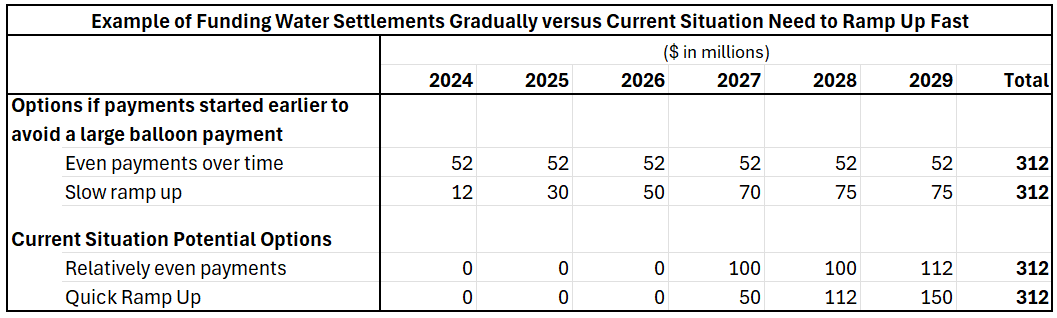

Providing additional funding for Indian water rights settlements is challenging when there are other major costs to be funded, as I’ve mentioned with Contract Support Costs and 105(l) leases, combined with a constrained budget. For context, $312 million is 7.8% of the Bureau of Indian Affairs budget. The cost will go up once final indexing (inflation payment) is calculated. The chart below shows that gradually building in water settlement costs can be more manageable, especially within the Interior and Environment appropriations bill, which is less likely to receive surges in funding than other appropriations bills. Given that no noticeable amounts have been appropriated, current options illustrate that a lot of money will be needed over the next three fiscal years.

Chart shows funding scenarios for an Indian water rights settlement with an enforceability date in in FY 2029.

Why are Indian water rights settlements important? Indian water rights settlements are critical for providing Tribal Nations with reliable, clean water, fulfilling the federal government's trust responsibility, enabling economic development, and resolving decades-old disputes with surrounding communities by securing quantified water rights and funding for infrastructure, benefiting water users by bringing certainty to resource management.

The lack of funding for the Hualapai settlement to date can also have a dampening effect on settlements pending authorization in Congress. The Federal government has not failed to enforce its actions for a water settlement in recent history. If this happens, technically the settlement falls apart, and the parties (Tribe, States, Federal government) must start over. Congress can also amend the current settlement to buy more time to gain the necessary funding. For a deeper background and a list of enacted settlements and settlements pending authorization, check out this Congressional Research Service report on Indian water rights settlements (July, 2025).

Who funds Indian Water Rights Settlements?

Settlement requirements are developed through negotiations among the Tribe, relevant State government, and Federal government, and then codified in Authorizing legislation. Funding requirements are generally paid for through the budgets of the Bureau of Reclamation and the Bureau of Indian Affairs. To date, and in general, Reclamation pays for project-based settlements, where Reclamation is building the project, and BIA pays for trust fund-based settlements, where funding is placed in a Trust Fund and earns interest until the Tribe builds out water projects or related authorized activities. As self-determination has increased, the recent trend has been for water rights settlements to be more trust fund-based, providing funding to the Tribes for project implementation.

Even though both bureaus are in the Department of the Interior, Reclamation is funded through the Energy and Water Appropriations Subcommittee, and BIA is funded through the Interior and Environment Appropriations Subcommittee. Arguably, the Energy and Water appropriations bill is better suited to absorb the new, high costs of enacted water rights settlements. Much of the Energy and Water bill is based on large projects that go up and down annually, leaving room for decision-making trade-offs among projects each year. By comparison, the Interior and Environment bill largely supports operational costs (salaries and benefits, predictable annual facility maintenance), which require more stable funding trajectories.

The FY 2026 Joint Explanatory Statement for the Energy and Water bill noted Bureau of Reclamation should spend at least $20 million in discretionary funding on water settlements. This funding is complemented by $120 million in mandatory funding that Reclamation receives each year out of its Indian Water Rights Settlement Fund. Given tight funding this year, it will be important to see the operating plan for how Reclamation will fund its settlements. This fund is authorized through FY 2029. BIA does not have a mandatory funding source for Indian water rights settlements.

Hail Mary Option? This is not impossible, but it is not prudent to wait. The $2.5 billion Indian Water Rights Settlement Completion Fund, included in the Bipartisan Infrastructure Law (PL 117-58), was one of those once-in-a-generation opportunities to address significant water rights settlement costs, such as the $1.9 billion Montana Water Rights Protection Act. It could be that there will be an alignment of stars, and a solution will be found for another source of mandatory funding, but there is no guarantee. Considerations for reauthorization for the Reclamation’s Water Right Settlement Fund, which expires at the end of FY 2029, could include providing the authority for funding at the level of the Interior Secretary, so funding could be used by either or both BIA or Reclamation for water rights settlements. However, that timeline does not work well for the Hualapai settlement unless Congress acts early. Another option would be to fund water settlements through the Energy and Water Appropriations Subcommittee, as discussed above.

Most likely, it may be left to the Interior and Environment subcommittee, which, I noted in previous posts, is also facing rising costs from other legally required payments, 105(l) Tribal leases, and Contract Support Costs - as well as operational needs. Whether through a discretionary funding increase or a new mandatory funding source, the Administration and Congress need a solution to these legally required payments – at some point, the creaky dam, pun intended, holding back growing needs and legal obligations will give.

Developing Perspective for FY 2026 Appropriations for Indian Affairs and Indian Health Service

With the Senate passage of an appropriations minibus including the Interior and Environment, Commerce and Energy and Water bills, it’s good to take a moment to both celebrate and reflect. First, congratulations to the House and Senate appropriators who were dealt a difficult hand and still pulled out a bipartisan bill.

Following the passage of a bill like the recent minibus, we look at the topline numbers. IHS is funded at $8.05 billion, an decrease of over $170 million due to low estimates for 105(l) and CSC in FY 2026. (See note at end of this blog post regarding budget scoring that can impact the calculation of the change from FY 2025). Indian Affairs is roughly flat at $4.0 billion, with no reductions overall to the major operating accounts, and a few targeted increases for law enforcement, natural resources and probate case processing. As a result, the initial reaction is often along the lines of, “Phew, the Administration’s significant proposed cuts were entirely rejected, and the bipartisan bill has some targeted increases here and there - looks pretty good given the situation.” But it’s also somewhat like celebrating the passage of a hurricane that largely missed us but left a good bit of flooding and long-term damage in other areas. It's important at times like these to step back and look where we are after muddling through a year of norm changes - especially with the FY 2027 President’s budget and appropriations process about to start in the next month or two.

I’m a fan of benchmarks, especially during times of significant change. I want to set some benchmark information about the budgets for IHS and IA Tribal Programs (think Bureau of Indian Affairs, Bureau of Indian Education, Bureau of Trust Funds Administration, Office of Assistant Secretary for Indian Affairs). They are impacted by the following trends:

(1) legally required payments for 105(l) Tribal Leases and Contract Support Costs are squeezing other programs, as I anticipated,

(2) costs from other agencies have been shifted to the Indian Affairs budget, and

(3) progress on Indian Water Rights Settlements is slowing.

These negative trends are increased because the last four budgets for Indian Affairs have been relatively flat or declining and have not included fixed costs to address annual inflationary increases. In the post below and two more to follow, I’ll set some benchmark information to inform upcoming decisions by the Administration and Congress. Next, there will be a set of posts on impacts from decreased transparency in the budget process.

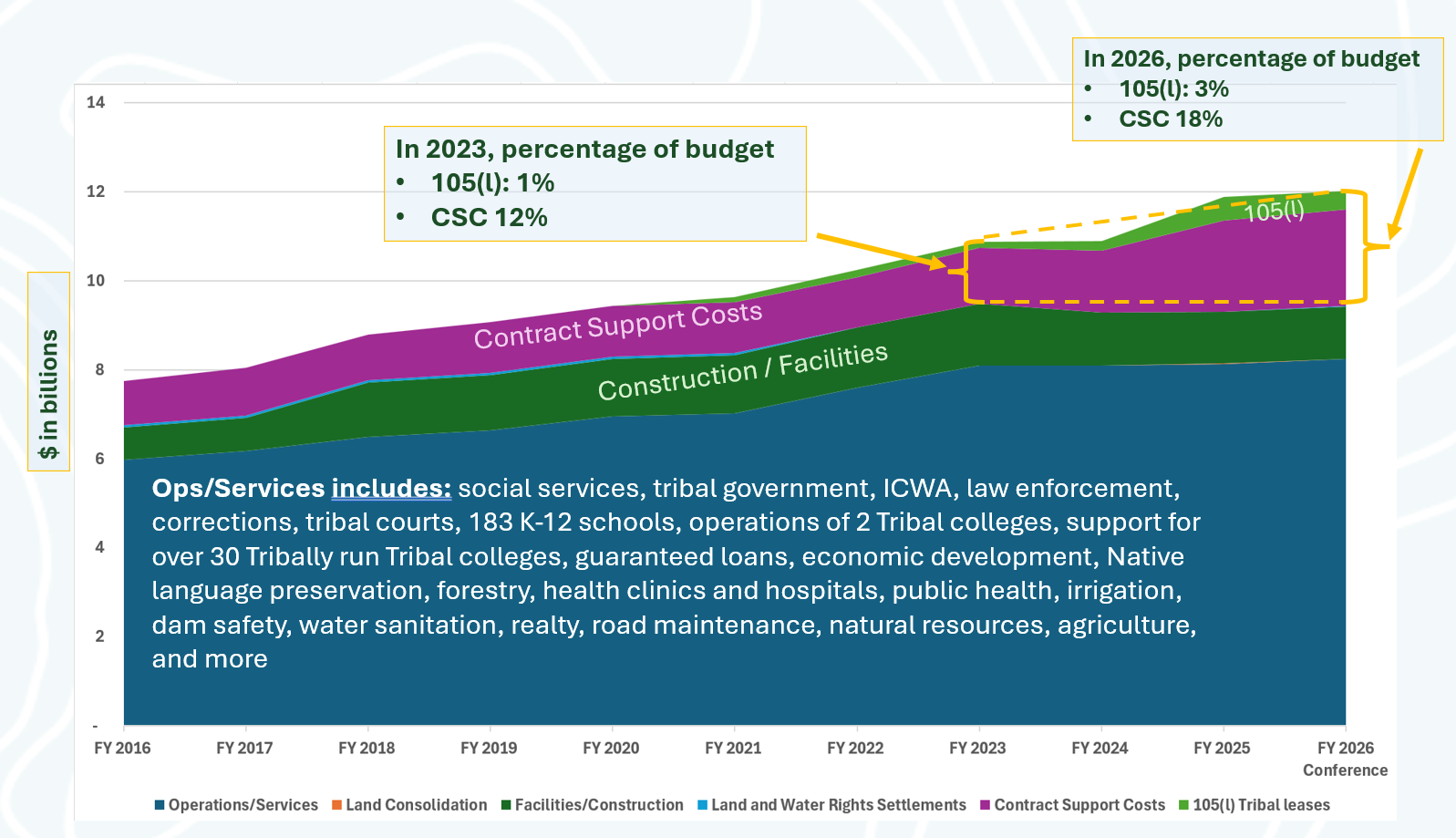

Issue 1: 105(l) Tribal Leases and Contract Support Costs (CSC) are squeezing out funding for other programs. Since FY 2022, funding at IHS and IA for operations and construction has declined as a percentage of their total budgets, while CSC and 105(l) grow as a percentage, as the chart below shows. The IHS and IA budgets totaled $10.9 billion in 2023 and now stand at $12 billion in 2026—a $1.14 billion increase. But here's the catch: the cost of 105(l) and CSC grew by $1.19 billion during those years, meaning other parts of the IA and IHS budgets, primarily facilities and construction, were reduced. During the same period, IA and IHS have not received fixed costs (inflation adjustments). Therefore, the agencies are largely treading water or underwater to address their Trust and Treaty responsibilities.

Long Term Trends for IA and IHS Budgets: 105(l) and CSC taking on Larger Share

The graph shows the long-term budget trend for the combined budgets of Indian Affairs and IHS, highlighting how growing in CSC and 105(l) is squeezing out other costs like construction and facilities management.

What are 105(l) Tribal leases and Contract Support Costs?

First, for folks who are newer to Indian Country here’s some basic info on 105(l) and CSC. Both are legally required payments under the Indian Self-Determination and Education Assistance Act (PL 93-638) and confirmed by Court decisions. Contract Support Costs are the necessary and reasonable costs associated with administering the contracts and compacts through which Tribes assume direct responsibility from IHS, BIA, and BIE. 105(l) Tribal leases are the necessary and reasonable costs the Federal Government must pay to Tribes and Tribal Organizations for facilities costs associated with contracted and compacted activities. While ISDEAA is nearly 50 years old, dedicated 105(l) appropriations only started in 2021. The section 105(l) program has grown significantly from executing three leases in 2019 to Tribes proposing more than 400 renewal or new leases by 2023. Outside of the legal requirement to pay these costs they are critical for advancing self-determination and economic development. CSC ensures Tribes have necessary administrative support to implement contracted programs. 105(l) has become the most innovative tool in a generation for Tribes to increase facility infrastructure investments to properly maintain current facilities and build new facilities for health care, education, public safety, and other services. For more information, review this Congressional Research Service report on Tribal Self-Determination Policies (see pages 12-13).

Why does the growth in these costs matter?

The FY 2026 conference agreement for the entire Interior and Environment appropriations bill totaled $42.5 billion, and was roughly $800 million below FY 2025 levels, about a two percent reduction. If budgets remain flat or decline, the challenge of funding legally required payments will increase. The need to address an increase in legally required payments can lead to overlooking the need to fund basic programs.

The U.S. Commission on Civil Rights’ Broken Promises report documents the underfunding of Trust and Treaty Requirements in detail. A good place to focus is IA Public Safety and Justice funding. BIA’s 2021Tribal Law and Order Act report, which calculated the need for law enforcement, estimated that BIA needed over $3 billion more than current funding levels to get to a proper level of funding for an adequate number of investigators and corrections staff and support for Tribal Courts.

On the Facilities and Construction side, high levels of deferred maintenance for BIA dams, irrigation systems, and law enforcement facilities, as well as BIE schools, are well documented. Funding for these programs has declined overall since FY 2022, while construction costs and facility needs have increased while older buildings remain in use. As a reference point, construction costs for nonresidential buildings rose 12.8% in 2022, followed by 5.6% in 2023 and 3.2% in 2024, a cumulative increase of approximately 22% since 2022 according to the Bureau of Labor Statistics. Further, the authorization for the Great American Outdoors Act Legacy Restoration Fund expired at the end of September 2025. As a result, Indian Affairs is no longer receiving $95 million a year for BIE school construction which has been critical for helping BIE keep up with increased construction costs. There does appear to be bipartisan support to reauthorize the Legacy Restoration Fund, maybe this summer, but funding will still be delayed for at least a year - if it is reauthorized.

The Tribal Leader Budget developed within the Tribal Interior Budget Council made an initial estimate of Indian Affairs budget needs of over $27 billion for FY 2026, as compared to $4 billion appropriated in FY 2026. This was not a full estimate of need, but it gives you a sense of the difference in scale between current funding levels and need. For IHS, there is a similar need for funding, albeit even greater. The National Tribal Budget Formulation Workgroup for the IHS budget has regularly estimated IHS needs at over $60 billion, compared with the $8 billion appropriated in FY 2026. These budget estimates don’t factor in another new cost to IA and IHS, legislation was recently enacted providing Federal recognition for the Lumbee Tribe. This is the ongoing tension, the Federal government continues to expand obligations to Tribes, but is having a hard time funding those obligations.

The pressure is not just on Indian Country programs. It's also important to note that the squeeze on 105(l) and CSC funding has ancillary effects on other programs in the Interior and Environment appropriations bill. The Interior-Environment Appropriations also funds other Interior bureaus like the National Park Service, Fish and Wildlife Service, the Environmental Protection Agency, and the Smithsonian Institution. Further, these budgets are affected by the rising costs of legally required payments.

So, what can be done? The ideal solution is to reclassify CSC and 105(l) as mandatory funding, so they no longer compete with discretionary investments. This was proposed by prior Administrations and included in previous Senate appropriations bill markups. So, while there has been momentum, it is a big lift in the current fiscal climate. Pressure may build, as it did with wildland fire suppression costs, to finally get to mandatory funding or a creative solution like the Wildland Fire Suppression Cap Adjustment, but there is no guarantee. A more incremental, but not easy, solution would be for Congress to ensure adequate discretionary funding increases for IA and IHS operational and facility programs.

Note about 105(l) and CSC budget scoring: The FY 2026 President’s budget and FY 2026 Appropriations statement of managers have inconsistent approaches to the FY 2025 budget score for CSC and 105(l). Since they are used more widely, and to reduce confusion, I updated my numbers to reflect the CBO estimates in the FY 2026 Appropriations statement of managers table of requirements. The drawback of updating the numbers is that I think the CBO estimates for FY 2026 are on the low end, and using CBO’s high 2025 estimates makes it look like there is a larger decrease than there really is.